Q2 2026: Enduring Principles

Reflections on True Wealth

Raphael Martorello

Managing Partner, Founder & CIO

What 250 Years Can Teach Us About Building Wealth

Over the Fourth of July weekend, our nation celebrated its 250th birthday, a milestone that caused me to pause and reflect.

For nearly two and a half centuries, the United States has been a remarkable experiment, not because we’ve always gotten things right, but because we’ve continued striving to build “a more perfect Union.” Our history has included war, economic crises, political division, and periods of profound uncertainty. Today’s challenges are numerous as well, from rising debt and political polarization to geopolitical tensions and rapid technological change. Yet throughout our history, America has demonstrated an extraordinary ability to adapt, innovate, and progress.

As we begin our nation’s next 250 years, we shouldn’t assume the future will simply take care of itself. Every generation inherits both the blessings and the responsibility of strengthening what came before. Long-term success requires thoughtful stewardship, disciplined decision-making, and the willingness to look beyond today’s headlines.

The same is true for building personal and family wealth.

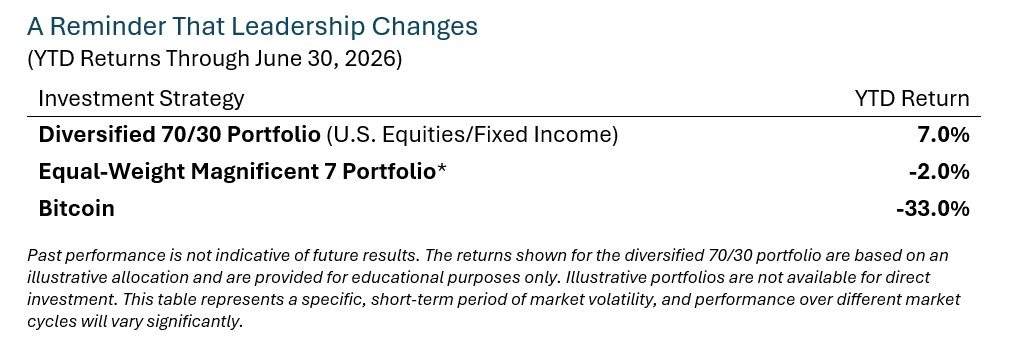

One of the greatest challenges investors face is resisting the temptation to believe that yesterday’s winners will automatically become tomorrow’s outperformers. The first half of 2026 provided a timely reminder of this challenge. Early-year market enthusiasm centered around the AI-focused Magnificent Seven stocks (Apple, Nvidia, Google, etc.) as well as the hottest cryptocurrencies after strong 2025 results. However, these investments were some of the worst performers during the first half of 2026, reminding us that market leadership changes, valuations matter, and concentrated bets can produce dramatically different outcomes than diversified portfolios.

The lesson isn’t that technology or digital assets are poor investments. Innovation will continue to create tremendous opportunities. Rather, it’s a reminder that successful investing has never been about chasing whatever is most popular at the moment. It’s about building a portfolio designed to endure changing market environments.

That kind of discipline rarely feels exciting in the moment. There will always be a new investment story promising outsized returns or a reason to believe that “this time is different.” Yet history repeatedly reminds us that wealth is built not by predicting every market cycle correctly, but by remaining patient, diversified, and focused on long-term goals.

As we reflected on our nation’s first 250 years, perhaps the greatest lesson isn’t simply how far we’ve come, but the values and institutions that have made that progress possible: hard work, managed risk, capital markets, togetherness, belief, discipline, resilience, and an enduring commitment to building something better for the next generation.

Similar principles apply to building wealth.

Neither a nation nor a portfolio succeeds by assuming yesterday’s success guarantees tomorrow’s. Both require discipline, thoughtful stewardship, and a long-term perspective.

Those are timeless principles—and they’re worth celebrating.

*Equal-Weight Magnificent 7 Portfolio assumes an equal investment in Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, and Tesla on January 1, 2026, held through June 30, 2026, with no rebalancing. Returns are based on publicly available market data through June 30, 2026.

Source: Publicly available market data through June 30, 2026. Portfolio calculations by the author.

Advisor Insights

Xavier Lewis

Financial Advisor

Sharing Wealth Across Generations: Choosing the Right Account for Children and Grandchildren

My name is Xavier, and for the past year and a half I've had the privilege of serving clients as a Financial Advisor with LotusGroup Advisors. While I've spent the last decade helping individuals and families navigate important financial decisions, I'm about to embark on a completely new journey of my own.

In just a few short days, my wife and I will welcome our first child - a son - to the world. As I prepare for this exciting new chapter, I've found myself thinking about the future and what I can do today to help set him up for success. I’d like to share with you some of these same ideas and strategies to help think beyond one’s own retirement. Whether you're a parent, grandparent, aunt, uncle, or simply someone who wants to invest in a child's future, there are several ways to begin building wealth for the next generation.

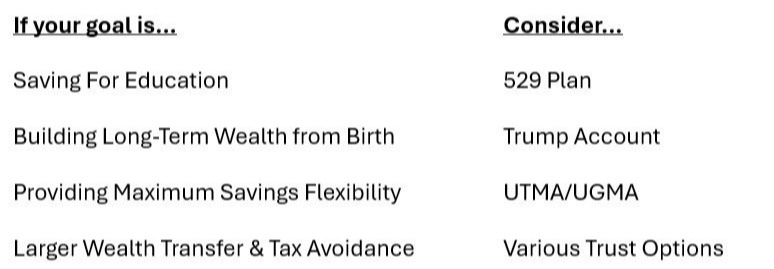

Recent legislation introduced a new option - the Trump Account - which joins two well-established planning tools: 529 College Savings Plans and UTMA/UGMA Custodial Accounts. Each serves a different purpose, and choosing the right one depends on your goals, flexibility, and long-term planning objectives.

Here's a closer look at each option.

Trump Accounts

Beginning in 2026, eligible children born during the qualifying period may have access to a new tax-advantaged investment account commonly referred to as a Trump Account. The goal is simple: give children a financial head start by encouraging long-term investing from birth and allow everyone to have a stake in our economy and system.

Potential Advantages

- Provides the opportunity for long-term investment growth through compounding over time.

- Family members, friends, and employers (subject to contribution rules) may contribute.

- Encourages long-term wealth accumulation rather than short-term spending.

- Certain children may receive an initial government-funded contribution if they meet eligibility requirements.

Potential Drawbacks

- Annual contribution limits apply.

- Funds generally cannot be accessed until adulthood.

- Withdrawals before certain ages or for non-qualified purposes may have restrictions or tax consequences.

- Because the program is new, future regulations and guidance will continue to evolve.

Net-Net: A Trump Account may be attractive for families focused on building long-term wealth over multiple decades.

529 College Savings Plans

For families with education in mind, a 529 plan remains one of the most widely used education savings vehicles.

Potential Advantages

- Investments grow tax deferred.

- Qualified education withdrawals are federal income tax-free.

- Many states offer state income tax deductions or credits for contributions.

- Funds can be used for college, graduate school, vocational programs, and certain K–12 education expenses.

- Recent rule changes allow some unused funds to be rolled into a Roth IRA for the beneficiary, subject to IRS requirements and lifetime limits.

Potential Drawbacks

- Designed primarily for education expenses.

- Non-qualified withdrawals may result in taxes and penalties on earnings.

- Investment flexibility is more limited than a standard brokerage account.

Net-Net: For families who expect education to be a significant future expense, a 529 plan continues to offer compelling tax advantages.

UTMA/UGMA Custodial Accounts

A UTMA (Uniform Transfers to Minors Act) or UGMA (Uniform Gifts to Minors Act) account offers the greatest flexibility.

Unlike education-specific accounts, these custodial accounts can hold investments that ultimately belong to the child.

Potential Advantages

Funds may be used for nearly any expense that benefits the child - not just education.

Wide variety of investment choices.

No contribution limits.

Simple way to transfer assets to the next generation.

Potential Drawbacks

Assets legally belong to the child and generally transfer to them upon reaching the age of majority (which varies by state).

The child gains full control of the assets once the account transfers.

Investment earnings may be subject to the "kiddie tax."

Assets may have a greater impact on college financial aid eligibility than some other account types.

Net-Net: A UTMA or UGMA account can be an excellent choice for families who value flexibility and are comfortable with the child eventually taking ownership of the assets.

There are also more complex trust options available including revocable and irrevocable trusts, generation-skipping trusts, etc.

So Which Option Is Best?

The answer depends entirely on your goals.

Of course, you aren’t limited to just one option and can combine several together.

Extra Credit Ideas

While gifting efficiently is part of the answer, the other part is in providing a financial education for your heirs so that they begin to develop solid behaviors for their futures. We encourage you to teach them:

1. Positive self-worth comes from being productive and creating value for others.

2. Spend less than you earn and practice delayed gratification to build lasting savings habits.

3. Become financially literate by reading books and blogs or listening to educational podcasts.

4. Live your family values. Wealth is simply a tool to support and express those values.

If these topics are interesting to you and/or you are considering gifting assets to children or grandchildren, I'd be happy to help evaluate which strategy, or combination of strategies, best fits your family's long-term financial plan.

If you have made it this far, I appreciate your interest and would be happy to talk more. Thanks again and as always, we encourage you to MAKE LIFE COUNT.

Public Market Highlights

Stephanie Schlemeyer, CFA

Partner, CCO & Director of Public Investments

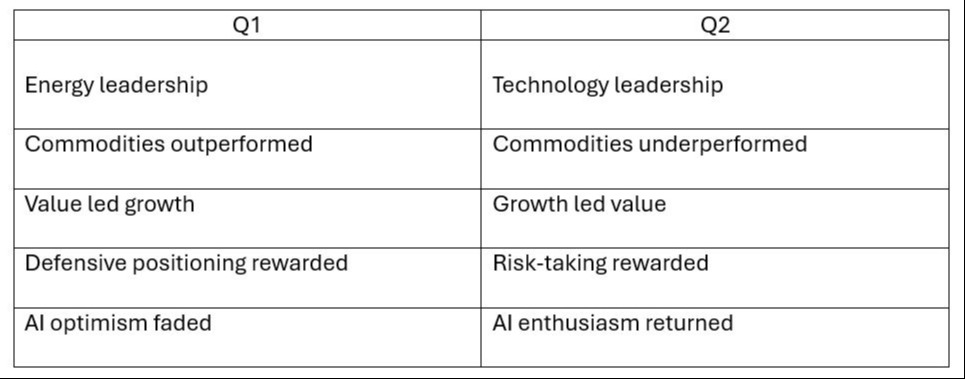

Jockeying for the Lead

The second quarter demonstrated just how quickly market leadership can change. After a difficult first quarter marked by inflation concerns, geopolitical uncertainty, and commodity strength, investor sentiment shifted rapidly, with attention returning to technology, artificial intelligence, and corporate earnings.

A few key themes shaped the quarter:

- Market leadership became increasingly concentrated during the quarter. While broad indexes posted strong returns, a relatively small group of AI-related technology companies accounted for a significant portion of those gains.

- Market participation was reasonably healthy. More than 60% of stocks remained above their long-term trend, suggesting the rally extended beyond just a handful of headline technology companies.

- International Equities were positive, but results were mixed. Emerging markets posted standout performance for the quarter. Emerging markets had a standout positive quarter, delivering 20%+ returns (ticker “EEM”) while foreign developed markets (ticker “EFA”) had positive returns but underperformed US equities.

Bottom line: Q2 reinforced one of investing's timeless lessons: leadership changes. Rather than chasing recent winners, maintaining a diversified portfolio, while rebalancing interim volatility can be an effective way to navigate ever-changing market environments.

What Happened in Your Portfolio

Tactical Strategies

Our Tactical strategies participated in the market's rebound while continuing to manage portfolios within their intended risk parameters. As investor optimism moderated near the end of the first quarter, we increased equity exposure to full allocation. Following the strong market recovery, and subsequent rise in investor optimism, we reduced equity exposure towards the end of April.

Global Strategies

Global portfolios benefited from broad equity market strength across both U.S. and international markets. While U.S. technology stocks led returns, diversification across regions and asset classes continued to provide balanced exposure as leadership evolved throughout the quarter.

Index Strategies

Index portfolios remained fully invested throughout the quarter and participated in the strong market advance. As always, portfolios were periodically rebalanced to maintain target allocations and appropriate risk levels.

Looking Ahead

The first half of 2026 served as another reminder that market leadership can change quickly. The themes that rewarded investors in Q1 were largely the same themes that lagged in Q2, and vice versa.

Rather than attempting to predict each rotation, we remain committed to a disciplined investment process focused on diversification, rebalancing, thoughtful risk management, and long-term investing. While short-term market leadership will inevitably change, our objective remains the same: help clients stay invested through changing market environments while remaining aligned with their financial goals and behavioral tolerances.

Private Market Update

Sam Redman

Director of Alternatives

Private Portfolio Update: The Short History of an Old Idea

Last quarter we wrote about why LotusGroup's private allocation is built differently from most of what gets called "private credit" in the news. We're returning to it this quarter because the story has evolved. Redemption pressure across several of the largest credit funds grew from Q1 to Q2, and the mechanism behind that pressure is worth understanding regardless of which investments you own.

America turns 250 this year. Organized public markets in this country go back to the 1790s, nearly as old as the country itself.¹ Lending against collateral is older still, predating modern banking entirely. "Private credit" as most investors now understand it is not old at all.

The mainstream version, direct lending to companies, often software and services businesses, is maybe a decade-and-a-half old at real scale. It grew out of a specific moment: banks pulled back from corporate lending after 2008 as new capital rules made those loans more expensive to hold, and the low rates that followed sent yield-starved investors straight into the gap banks left behind. That loan is backed by a company's future cash flow and growth projections. If the company stumbles, repayment depends on the fund finding a buyer for the loan, or on the company's value holding up, neither of which is guaranteed on any given day.

This is not a hypothetical risk. Apollo's largest retail-facing credit fund, a $26 billion vehicle, saw withdrawal requests reach roughly 17% in the second quarter of 2026, up from around 11% the prior quarter, and again capped payouts at its contractual 5% limit.² The pressure was not isolated to one manager. Investors across four large credit funds, including ones run by Blackstone and BlackRock, sought to redeem about $12 billion in the second quarter, up from $7.7 billion in the first, according to data from investment bank Robert A. Stanger & Co.³

Asset-backed lending, the kind LotusGroup has focused on for a decade, is a different animal. Lending secured by receivables, equipment, leases, or real estate is one of the oldest forms of finance there is. What's new is only the wrapper, the fact that a fund can now package it for investors who had limited, if any, access before. Loans are backed by something specific and appraisable, not a projection.

That's why some funds are gating and others aren't. A fund that has to sell loans to pay investors back runs into a very human problem: if enough people suspect others might redeem first, everyone redeems first, whether or not anything is actually wrong with the loans. A fund that gets repaid by borrowers on a set schedule, and simply passes that cash along, has nothing to sell and nothing to run from.

A recent example: in Q1 2026, LotusGroup co-invested in a bridge loan secured by a hotel property in Malibu, California. The loan sits in first mortgage position on the real estate, at roughly half the property's appraised value, backed further by a personal guarantee from the operator. There is a specific, appraised asset behind that loan, not a projection about where a business might be in three years.

That's the distinction worth remembering the next time you see the words "private credit" in a headline.

"Private credit" as a general term covers much more than most people initially assume. Differences in collateral, structure, duration, and liquidity can mean very different outcomes for an investor, and understanding those differences matters far more than the label itself.

Two hundred and fifty years in, American markets have rewarded the same thing again and again: patience, real collateral, and structures built to last through a cycle, not just to raise capital ahead of one. That's not a new idea, and it's not one we invented. It's simply the one we've built LotusGroup's private portfolio around, and the one we intend to keep building around.

-------------------------------------------------------------

¹ Source: NYSE, "History of NYSE." https://www.nyse.com/history-of-nyse

² Source: CNBC, "Apollo curbs withdrawals after exit requests hit 17%, reigniting fears over private credit liquidity," June 23, 2026. https://www.cnbc.com/2026/06/23/apollo-private-credit-fund-withdrawals-redemptions.html

³ Source: The Wall Street Journal, "Even More Investors Want Out of Private Credit," citing data from Robert A. Stanger & Co. https://www.wsj.com/finance/investing/even-more-investors-want-out-of-private-credit-4c225a9c

This commentary is provided for informational and educational purposes only and should not be construed as specific investment, legal, tax advice, or a recommendation to buy or sell any security. References to specific securities, tickers (including EEM and EFA), sectors, or asset classes are for illustrative purposes only, represent broad market segments, and do not reflect the actual performance of any specific client account or portfolio. Investing involves risk, including the possible loss of principal. Tactical allocation strategies do not guarantee a profit or protect against loss in a declining market. Asset-backed investments and private portfolios involve unique risks, including borrower default, collateral impairment, illiquidity, and valuation uncertainty. While collateral may reduce certain risks, it does not guarantee repayment or protect against loss, and there can be no assurance that any investment objective will be achieved. The case studies and examples provided are for educational illustration only; the experience of any individual fund, investment, or strategy should not be viewed as representative of the broader private credit market, which features a wide variety of investment structures, risk profiles, and liquidity characteristics. Past performance is no guarantee of future results.